- Salesforce beat consensus on Q2 earnings, but that wasn’t enough for investors.

- The Agentforce AI product is growing but not enough to raise full-year guidance.

- Expect CRM stock to continue drifting lower into the $212 to $240 demand window.

- Plenty of poor employment data on Thursday bodes poorly for Friday’s NFP print.

Investors were looking for hefty results late Wednesday, but Salesforce’s (CRM) simply decent quarterly print was not up to snuff. Shares of the customer relationship management software provider gave up over 7% at the start on Thursday, and now CRM is moving back toward its yearly lows.

The wider stock market has eased into slight gain in the late morning trade on Thursday — with the Dow Jones Industrial Average (DJIA), S&P 500 (SPX) and NASDAQ Composite (IXIC) all advancing about 0.3%. The market is a bit distracted due to Friday’s Nonfarm Payrolls (NFP) report for August. The worry is that it could be a repeat of the disastrous July print one month ago, especially following a slew of poor US employment readings on Thursday.

The ADP Employment Change report gave a figure of 54K net new jobs in August that was below the 65K consensus. The Challenger Job Cuts survey showed nearly 86K US layoffs in August, well above the 62K seen in July. Initial Jobless Claims for the previous week rose to 237K, above the 230K consensus.

Salesforce back in the doldrums after poor AI results

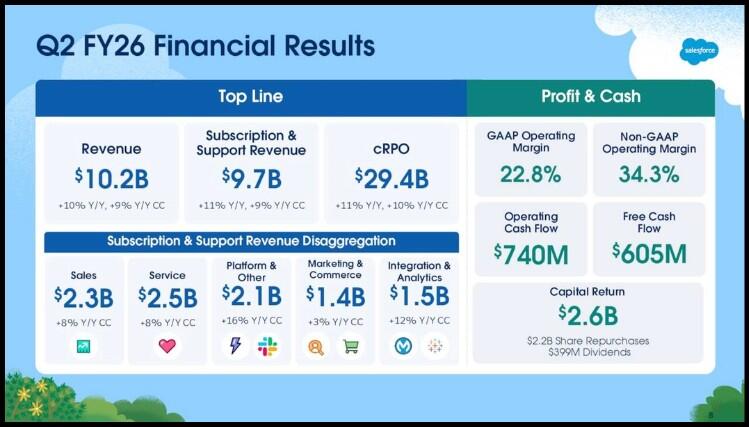

It’s too bad for Salesforce that the market only cares about its AI progress. That’s because the overall second-quarter result at Salesforce was quite decent. The company reported adjusted earnings per share (EPS) of $2.91, 13 cents better than the consensus. Revenue of $10.24 billion also bested the average projection by $100 million.

CEO Marc Benioff placed Q3 guidance between $10.24 billion and $10.29 billion, which amounts to a 0.5% QoQ gain, which analysts found unimpressive.

“Lack of a FY raise on a decent 2Q suggests less upside [the rest-of-year than previously expected],” Wells Fargo analyst Michael Turrin wrote in a note to clients. “Remain balanced until greater signs of a catalyst emerge, w/ Agentforce uptake proving slower than anticipated (ARR disclosure not given).”

Q2 FY26 earnings results from Salesforce.com

Evercore ISI analyst Kirk Materne, whose $350 price target is far about Turrin’s $265, added that, “[W]e did not see this quarter as the ‘unlock’ for the bull case.” Still, Materne thinks Salesforce stock remains in a holding pattern until AI products like Agentforce begin paying dividends.

The Agentforce platform, which allows corporate customers to build their own branded AI customer service agents, did see a rise in paying customers to 6,000. But analysts said that the company’s full-year guidance for revenue between $41.1 billion and $41.3 billion demonstrated that the major gains in AI wouldn’t materialize in the back half of the year.

Salesforce also raised their buyback scheme by $20 billion, which should help to stabilize the share price.

Salesforce stock chart

Salesforce stock has risen out of the wide support region on Thursday between $212 and $240 that has often worked to fortify sell-offs in CRM. But since the stock fell back into that region after earnings, it signals there isn’t much optimism in the near future.

The August 12 low near $226 beckons as does the $212 level that held up shares during the May 2024 sell-off. Bears will surely notice that CRM bounced lower off the 50-day Simple Moving Average (SMA) twice in the past two months. While the stock is getting cheap at these levels, an even better entry point is likely to come.

CRM daily stock chart

Other Articles

No Comment! Be the first one.